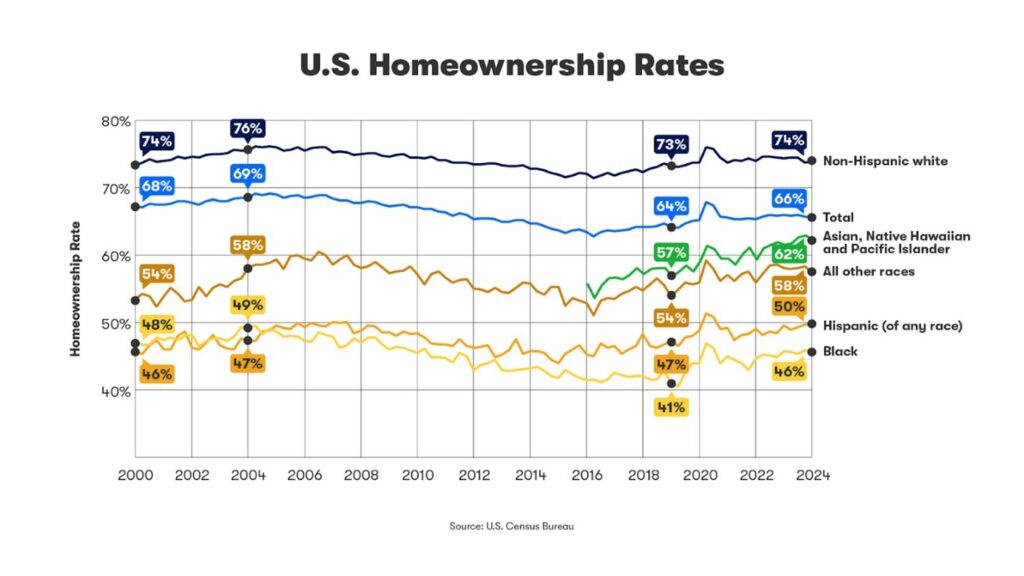

According to new data from Zillow, the homeownership rate for Black households has grown faster than average since 2019, but it’s still below the high-water mark reached in 2004, before the Great Recession.

Zillow analyzed 2023 Home Mortgage Disclosure Act data, and found that insufficient credit is a major factor holding many Black households back from homeownership, as nearly one in four mortgage applications from Black borrowers (24%) are denied. That total is nearly twice the rate of all applicants (12.6%), and far higher than the one-in-10 denial rate for white applicants. Of those mortgages denied Black applicants, more than 43% are turned down due to credit history–the most common reason given. That’s a higher rate than in past years, and also when compared to 32% of denials for white applicants.

“While discriminatory policies like redlining have long been outlawed, the damage from these historic practices is still felt today. Many communities once barred from accessing credit are now finance deserts, with few traditional financial institutions, making it harder to build credit and buy a house,” said Zillow Senior Economist Orphe Divounguy. “That’s why it’s so important to expand credit access. Allowing rent payments to count in credit scores is one example of how to move the industry forward.”

A disparity remains

Nearly 46% of Black households presently own their home, an improvement from a low point of 43% in 2019, but still down from a 49.7% peak ownership rate reached in 2004, before the Great Recession, and far off from the 74% rate for white households.

Many Black households have been left out of major wealth gains during that time. Since the Black homeownership rate peaked in 2004, U.S. home values have more than doubled, rising 117%.

While the gap between white homeownership rates and those of Black and Hispanic households has diminished since 2019, an alarming deficit remains. The single largest asset for most homeowners is their home, which remains a major means of building wealth and passing it on to the next generation. Zillow Research found a $3 trillion wealth gap between Black and white families, with nearly 40% of the gap—$1.18 trillion—could be credited to disparities in home values and ownership.

Despite rising faster than average since 2019, Black-owned home values are still far lower than average. If the typical home was worth $1, Black-owned homes would be worth 85 cents and white-owned homes worth $1.03.

Leveraging tech to address housing inequality

Rent payments made to landlords on the Zillow Rentals platform can now count toward a renter’s credit score. Zillow is pushing for systemic, national changes on this front, advocating for bipartisan legislation that would encourage property owners and utility and telecom providers to report payment data to credit reporting agencies. This would give consumers who pay their bills on time the chance to build a positive credit history.

Home shoppers can see what down payment assistance programs they could qualify for on every Zillow listing, saving shoppers the hassle of looking up their eligibility on various government websites.

Continuing its investment in new technology to address biases and inequalities in housing, Zillow recently released the open-source Fair Housing Classifier, a tool that establishes guardrails to help prevent historic biases from resurfacing in real estate conversations powered by large language model (LLM) technology.