The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey reveals that the total number of loans now in forbearance increased by three basis points in November 2024 relative to October 2024, from 0.47% to 0.50 (as of November 30, 2024). According to MBA’s estimate, 250,000 homeowners are currently in forbearance plans, as the nation’s mortgage servicers have provided forbearance to approximately 8.5 million borrowers since March 2020.

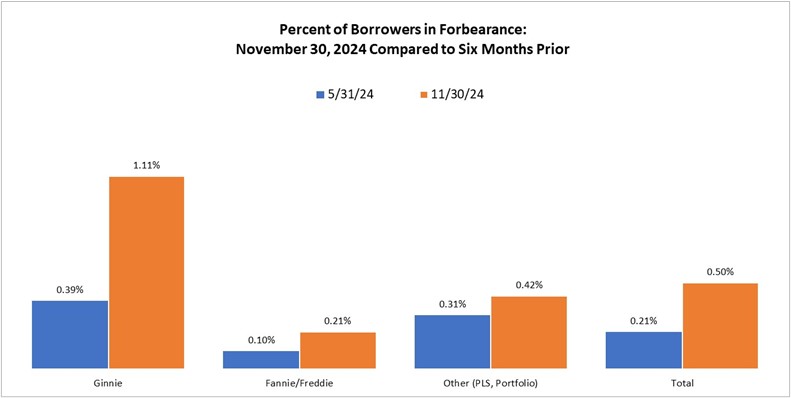

The share of Fannie Mae and Freddie Mac (GSE) loans in forbearance increased one basis point from 0.20% to 0.21% in November 2024. Ginnie Mae loans in forbearance increased by five basis points from 1.06% to 1.11%, and the forbearance share for portfolio loans and private-label securities (PLS) decreased one basis point from 0.43% to to 0.42%.

“The overall mortgage forbearance rate increased three basis points in November and has now risen for six consecutive months,” said Marina Walsh, CMB, MBA’s VP of Industry Analysis. “By investor type, Ginnie Mae loans are showing the greatest variance, with an increase of 72 basis points over the six-month period. That is compared to 11 basis points for Fannie Mae and Freddie Mac Loans, and portfolio and PLS loans, respectively.”

Key Findings of MBA’s Loan Monitoring Survey

- By reason, 51.3% of borrowers are in forbearance for reasons such as a temporary hardship caused by job loss, death, divorce, or disability. Another 46% are in forbearance because of a natural disaster. Less than 2.8% of borrowers are still in forbearance because of COVID-19.

- By stage, 71.4% of total loans in forbearance are in the initial forbearance plan stage, while 16.5% are in a forbearance extension. The remaining 12.1% are forbearance re-entries, including re-entries with extensions.

- Total loans serviced that were current (not delinquent or in foreclosure) as a percent of servicing portfolio volume (#) was 95.22% in November 2024, down 22 basis points from 95.44% the prior month (on a non-seasonally adjusted basis), and down 49 basis points from one year ago.

- The five states with the highest share of loans that were current as a percent of servicing portfolio: Washington, Idaho, Alaska, Oregon, and Colorado.

- The five states with the lowest share of loans that were current as a percent of servicing portfolio: Louisiana, Mississippi, Indiana, West Virginia, and Alabama.

- Total completed loan workouts from 2020 and onward (repayment plans, loan deferrals/partial claims, loan modifications) that were current as a percent of total completed workouts decreased to 66.47% in November 2024, down 200 basis points from 68.47% the prior month and down 501 basis points from one year ago.

“There is some weakening in performance of servicing portfolios and loan workouts compared to one year ago,” added Walsh. “In the wake of natural disasters and slowing in the labor market, borrowers with government loans tend to be impacted more than conventional borrowers.”

MBA’s monthly Loan Monitoring Survey covers the period from November 1 through November 30, 2024, and represents 62% of the first-mortgage servicing market (30.9 million loans).