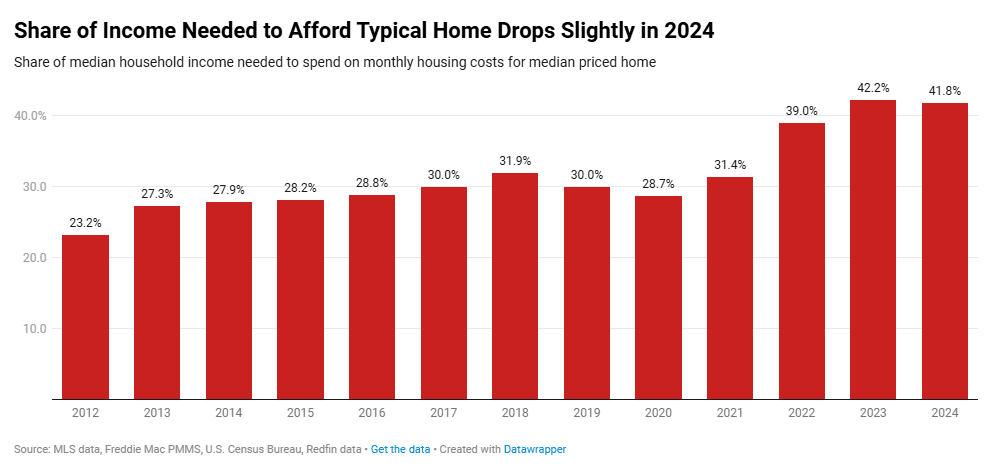

According to a new study from Redfin, a household making a median U.S. income of $83,782 in 2024 would’ve had to spend 41.8% of their earnings on monthly housing costs if they bought a $429,734 median-priced U.S. home. That’s a slight improvement from 42.2% in 2023, but is considerably less affordable than the typical share of 30% or lower recorded throughout the 2010s.

“Affordability improved ever so slightly this year because wage growth outpaced the growth in monthly housing payments,” said Redfin Senior Economist Elijah de la Campa. “But that’s not to say buying a home became affordable. For many Americans, buying a home remains more out of reach than ever and that’s unlikely to change anytime soon. Even with inventory trending upwards, we still expect prices to continue rising in 2025 due to a lack of homes for sale—pushing more would-be homebuyers to rent instead.”

How Much Do Americans Need to Earn?

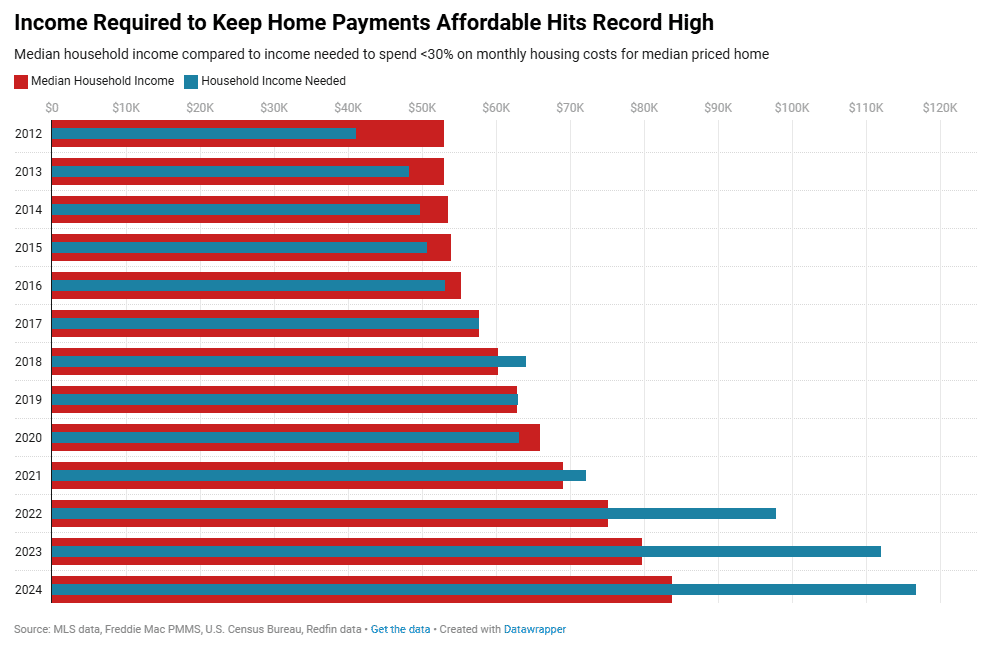

In 2024, a homebuyer needed to earn an annual income of at least $116,782 if they wanted to spend no more than 30% of their earnings on monthly housing payments for the median-priced home. That’s a record high, and is $33,000 more than the typical household makes in a year.

The median monthly housing payment for homebuyers hit a record of $2,920 in 2024, rising 4.3% from 2023 and 86% from 2019. In contrast, wages have grown around 4% year-over-year throughout 2024. The slight improvement in affordability this year is mainly due to the slightly lower average mortgage rate (6.72%), compared to 2023 (6.81%). It was the fourth consecutive year in which the income needed to keep home payments affordable was higher than the median household income.

Affordability Trends Nationwide

In Austin, Texas, a household making the $103,717 median income in 2024 would have had to spend 39.6% of their earnings on monthly housing costs if they bought a $444,928 median-priced home there, down from 42.8% in 2023. That was the biggest improvement in affordability among the 50 most populous U.S. metropolitan areas.

In the Lone Star State, housing construction has boomed in recent years, especially during the pandemic, when remote workers flocked to more affordable regions in the Sun Belt. With inventory up and demand easing, home prices in the region are starting to fall, leading to an improvement in affordability.

Following Austin, the next four metros in order of improved affordability were:

- San Antonio, Texas (-2.3 ppts to 35.4% of household income)

- Dallas, Texas (-2 ppts to 38.9%)

- Fort Worth, Texas (-1.6 ppts to 36.7%)

- Portland, Oregon (-1.4 ppts to 45%)

On the other end of the spectrum, in Anaheim, California, a household making the $121,925 median income in 2024 would have had to spend 75.9% of their earnings on monthly housing costs if they bought the $1,165,965 median-priced home—up 71.8% in 2023—the biggest jump among the top 50 metros. Anaheim was followed by:

- Chicago, Illinois (+2 ppts to 34.7%)

- Miami, Florida (+1.7 ppts to 63.1%)

- Newark, New Jersey (+1.6 ppts to 48.8%)

- San Jose, California (+1.5 ppts to 73.9%)

Housing affordability worsened in those metros largely because U.S. home prices soared. Anaheim posted a 12.4% increase in home prices in 2024—the biggest jump among the major metros—while Chicago (8.6%), Miami (7.9%), Newark (11.3%) and San Jose (8.6%) all posted gains higher than the national level (4.8%).

Where Are the Least Affordable Metros Located?

The five least affordable major metros are all in California. In Los Angeles, someone making the median income in 2024 would have had to spend 77.6% of their earnings on monthly housing costs if they bought the median priced home.

Los Angeles was followed by:

- San Francisco, California (76.2%)

- Anaheim, California (75.9%)

- San Jose, California (73.9%)

- San Diego, California (67.3%)

The least affordable non-California metro is New York, where homebuyers on the median income would need to spend 65.9% of their earnings on housing costs.

In many areas, buying a home remains affordable. Using the rule of thumb that a homebuyer should spend no more than 30% of their income on housing payments—especially in the Rust Belt, where the median home price remains under $300,000 in a number of metros. In Pittsburgh, someone making the median income in 2024 would’ve had to spend 25.3% of their earnings on monthly housing costs if they bought the median priced home—the lowest share among the metros Redfin analyzed and below the 30% threshold. Next came Detroit (25.5%); St. Louis (26%); Cleveland (26.4%); and Warren, Michigan (28%).

Click here for more on Redfin’s report on U.S. homebuyer affordability in 2024.