The Mortgage Bankers Association (MBA) has released its monthly Loan Monitoring Survey, the final report for 2024, revealing that the total number of loans now in forbearance decreased by three basis points from 0.50% of servicers’ portfolio volume in the prior month to 0.47% as of December 31, 2024.

According to MBA’s estimate, 235,000 homeowners are currently in forbearance plans, and mortgage servicers have provided forbearance to approximately 8.5 million borrowers since March 2020.

The share of Fannie Mae and Freddie Mac (GSE) loans in forbearance decreased two basis points from 0.21% to 0.19% in December 2024. Ginnie Mae loans in forbearance decreased by four basis points from 1.11% to 1.07%, and the forbearance share for portfolio loans and private-label securities (PLS) decreased two basis points from 0.42% to 0.40%.

“The overall mortgage forbearance rate decreased slightly in December as some borrowers got back on track following last fall’s severe weather in the Southeast,” said Marina Walsh, CMB, MBA’s VP of Industry Analysis. “Even with the slight decrease, the level of forbearance is higher than it was six months ago across all loan types, and the performance of servicing portfolios and loan workouts has weakened.”

Key Findings of MBA’s Loan Monitoring Survey

Loans in forbearance as a share of servicing portfolio volume (#) as of December 31, 2024 include:

- Total: 0.47% (previous month: 0.50%)

- Independent Mortgage Banks (IMBs): 0.54% (previous month: 0.58%)

- Depositories: 0.38% (previous month: 0.39%)

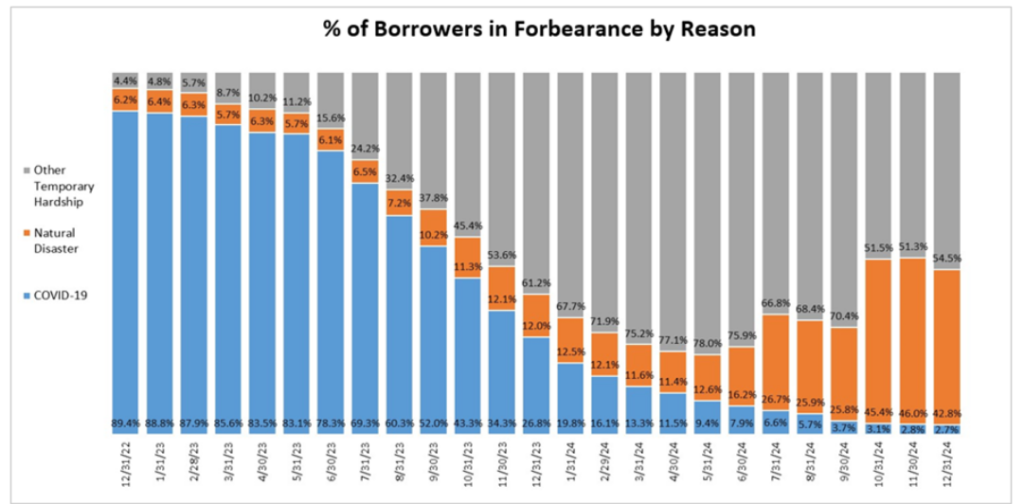

By reason, 54.5% of borrowers were in forbearance for reasons such as a temporary hardship caused by job loss, death, divorce, or disability. Another 42.8% were in forbearance because of a natural disaster. Less than 2.7% of borrowers were still in forbearance because of COVID-19.

By stage, 70.5% of total loans in forbearance were in the initial forbearance plan stage, while 16.8% are in a forbearance extension. The remaining 12.7% are forbearance re-entries, including re-entries with extensions.

Total loans serviced that were current (not delinquent or in foreclosure) as a percentage of servicing portfolio volume (#) was 95.05% in December 2024, down 17 basis points from 95.22% the prior month (on a non-seasonally adjusted basis), and down 39 basis points from one year ago.

The five states with the highest share of loans that were current as a percentage of servicing portfolio:

- Washington

- Idaho

- Alaska

- Oregon

- Colorado

The five states with the lowest share of loans that were current as a percentage of servicing portfolio:

- Alabama

- West Virginia

- Indiana

- Mississippi

- Louisiana

Total completed loan workouts from 2020 and onward (repayment plans, loan deferrals/partial claims, loan modifications) that were current as a percentage of total completed workouts decreased to 65.39% in December 2024, down 88 basis points from 66.27% the prior month and down 900 basis points from one year ago.

“At year end, almost 43% of borrowers in forbearance were there due to a natural disaster,” added Walsh. “Given the disruption and devastation caused by the California wildfires, that share will likely move higher in the months ahead, as homeowners turn to forbearance to allow time to navigate their recovery process.”

As noted by Walsh, the recent wildfires in the Los Angeles area will surely impact forbearance totals as 2025 begins. Redfin has found that roughly one of every seven (14%) homes within the perimeters of the Palisades and Eaton fires in the Los Angeles area have been destroyed or damaged. That’s a total of 6,354 homes; of those, 5,449 (86%) were destroyed, and 905 (14%) were damaged.

CoreLogic also announced its preliminary residential and commercial loss estimates for the Eaton and Palisades Fires, and according to this data, ongoing losses from the Los Angeles wildfires are estimated to be between $35 to $45 billion, as both fires were less than 50% contained as January 16. CoreLogic’s analysis of both residential and commercial properties accounts for both fire and smoke damage as well as demand surge, debris removal, clean up and Additional Living Expenses (ALE). The majority of losses are to residential properties. Many of the potentially impacted properties are high value homes, so even moderate damage from the fires or smoke could result in costly claims.

Click here for more on MBA’s monthly examination of forbearance trends.