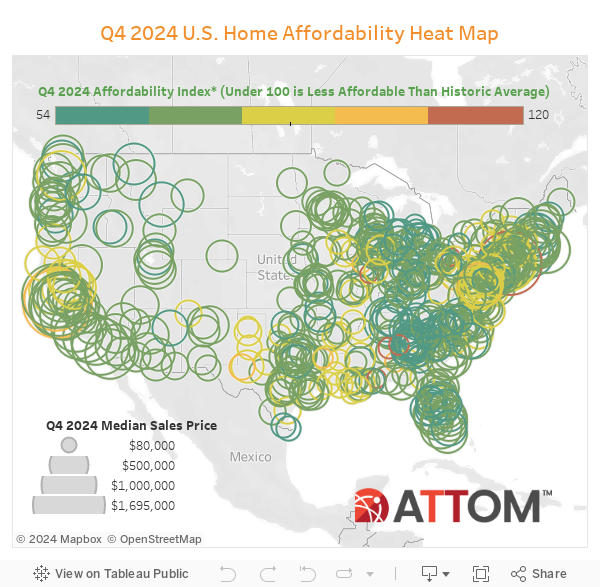

According to ATTOM’s Q4 2024 U.S. Home Affordability Report, median-priced, single-family homes and condos remain less affordable compared to historical averages in 98% of counties around the nation with enough data to analyze. The latest trend continues a three-year pattern of homeownership requiring historically large portions of wages, as U.S. home prices keep reaching new heights.

ATTOM’s study shows that major expenses on median-priced homes currently consume 34% of the average national wage—an increase of more than one percentage point both quarterly and annually, pushing the figure even farther above the common 28% lending guideline preferred by lenders.

The downturns in current and historic affordability represent the latest measures of how homeownership remains a financial stretch for the average U.S. worker, with the national median home price having climbed to $364,750 in Q4 and mortgage rates, while declining, remain edging near the 7%-mark. Combined, those forces are helping to keep the ratio of ownership expenses to wages in the unaffordable range.

Q4 trends also have reversed a slight improvement during Q3 of this year that had signaled a possible step in the right direction for homeowners. The portion of average wages nationwide required for typical mortgage payments, property taxes and insurance now stands almost 13 points beyond a low point reached early in 2021, right before home-mortgage interest rates shot up from the lowest levels in decades.

“The U.S. housing market continues to generate great profits for most home sellers, but also more and more financial stress for would-be buyers. Average workers now must shell out a larger portion of their wages for major homeownership expenses than at any time since right before the housing market tanked in the late 2000s,” said Rob Barber, CEO for ATTOM. “Despite recent declines in mortgage rates, down payments on typical home purchases have reached four times the average national wage.”

The report determines affordability for average wage earners by calculating the amount of income needed to meet major monthly home ownership expenses—including mortgage payments, property taxes and insurance—on a median-priced single-family home and condo, assuming a 20% downpayment and a 28% maximum “front-end” debt-to-income (DTI) ratio. That required income is measured against annualized average weekly wage data from the U.S. Bureau of Labor Statistics.

Compared to historical levels, median homeownership costs in 556 of the 566 counties analyzed in Q4 of 2024 are less affordable than in the past. That is virtually unchanged from both Q3 of 2024, and Q4 of 2023.