With the average 30-year mortgage rate in the U.S. lingering near the 7% mark, homeowners have learned to come to grips with an ever-shifting housing market.

However, high rates alone do not explain why customer satisfaction scores for mortgage servicers are significantly lower—and declining—than they are for mortgage originators.

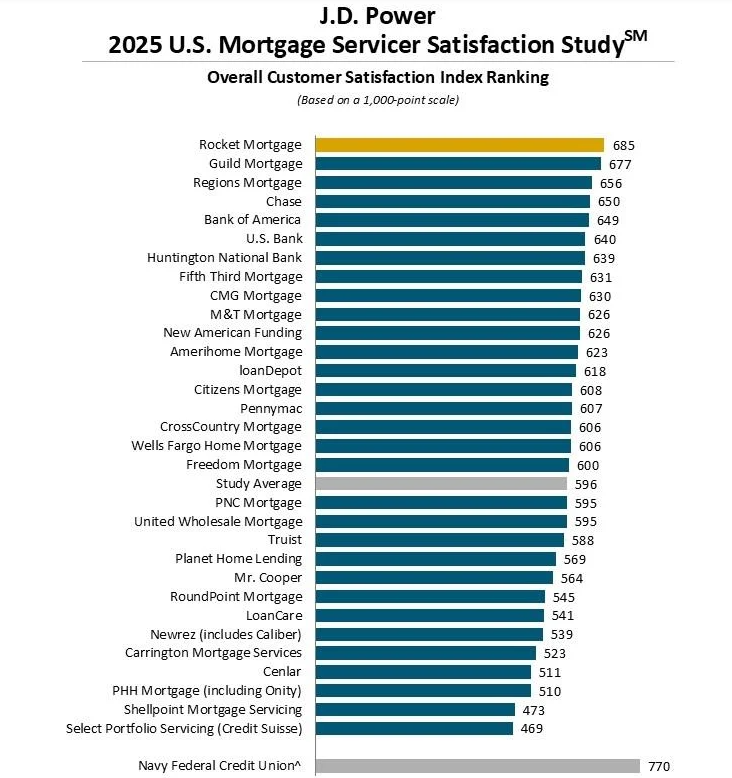

According to the latest J.D. Power 2025 U.S. Mortgage Servicer Satisfaction Study, customer satisfaction with mortgage servicers has dipped in 2025, with an average satisfaction score that is now 131 points (on a 1,000-point scale) lower than the average score for mortgage originators. Increasingly, the difference between the two comes down to effective communication and customer service.

Among the nation’s top mortgage servicing firms, Rocket Mortgage ranked highest among with a score of 685, followed by Guild Mortgage at 677, Regions Mortgage at 656, Chase at 650, Bank of America at 649, U.S. Bank at 640, Huntington National Bank at 639, Fifth Third Mortgage at 631, CMG Mortgage at 630, and M&T Mortgage and New American Funding tied at 626 rounding out the top 10.

“There is a significant disconnect in the mortgage customer journey that’s reflected in the fact that satisfaction with mortgage origination is reaching record highs at the same time that satisfaction with mortgage servicing is reaching all-time lows,” said Bruce Gehrke, Senior Director of Lending Intelligence at J.D. Power. “Part of this is driven by the economy. Rates are still high, volumes are down, consumer financial health is strained, and the industry is struggling to maintain high levels of customer engagement and personalization throughout the servicing experience. However, without delivering on important loyalty and advocacy metrics, servicers could be headed for some challenges down the road when volumes pick back up again.”

Key Takeaways

Conducted from May 2024 through May 2025, the U.S. Mortgage Servicer Satisfaction Study measures customer satisfaction with the mortgage servicing experience in six dimensions (in order of importance):

- Level of trust

- Makes it easy to do business with

- Keeps me informed and educated

- People

- Resolving problems or questions

- Digital channels.

Results from the study are based on responses from 15,912 customers who have been with their current mortgage loan servicer for at least one year.

Some highlights and takeaways from the U.S. Mortgage Servicer Satisfaction Study include:

- A fragmented customer journey: Overall customer satisfaction with mortgage servicers is 596, which is down 10 points from the 2024 study. Customer satisfaction with mortgage servicers declines across all dimensions year-over-year. This decline stands in contrast to customer satisfaction with mortgage originators, which reached a score of 727 in the J.D. Power 2024 U.S. Mortgage Origination Satisfaction Study.

- Service quality and responsiveness play significant role in customer loyalty: While better interest rates and lower costs and fees are cited most frequently by customers as a reason to switch mortgage providers, service quality, and responsiveness can be equally powerful drivers of customer loyalty and retention. Customers note that better/improved customer service (51%); easy access to loan information (36%); and flexible ways to make a mortgage payment (27%) were among the top reasons to switch mortgage companies.

- Communication breakdown: Despite efforts to deliver more effective communications, just 31% of mortgage servicer customers gave an excellent or perfect rating to their servicer for messaging that got their attention. Attention-getting is rated higher when there is a level of personalization added to the communication. Among those who have received personalized communications, account alerts are the most frequently recalled form of communication at 46%. Just 32% of customers give their mortgage servicer a high overall communication rating, down five percentage points from 2022.

- Satisfaction decreases as escrow costs rise: Escrow costs are rising nationwide, with 57% of mortgage servicer customers experiencing an increase in escrow costs this year. Overall satisfaction is 67 points lower, on average, among those who experienced an escrow cost increase than among those who experienced no change.

Click here for more on the latest J.D. Power 2025 U.S. Mortgage Servicer Satisfaction Study.