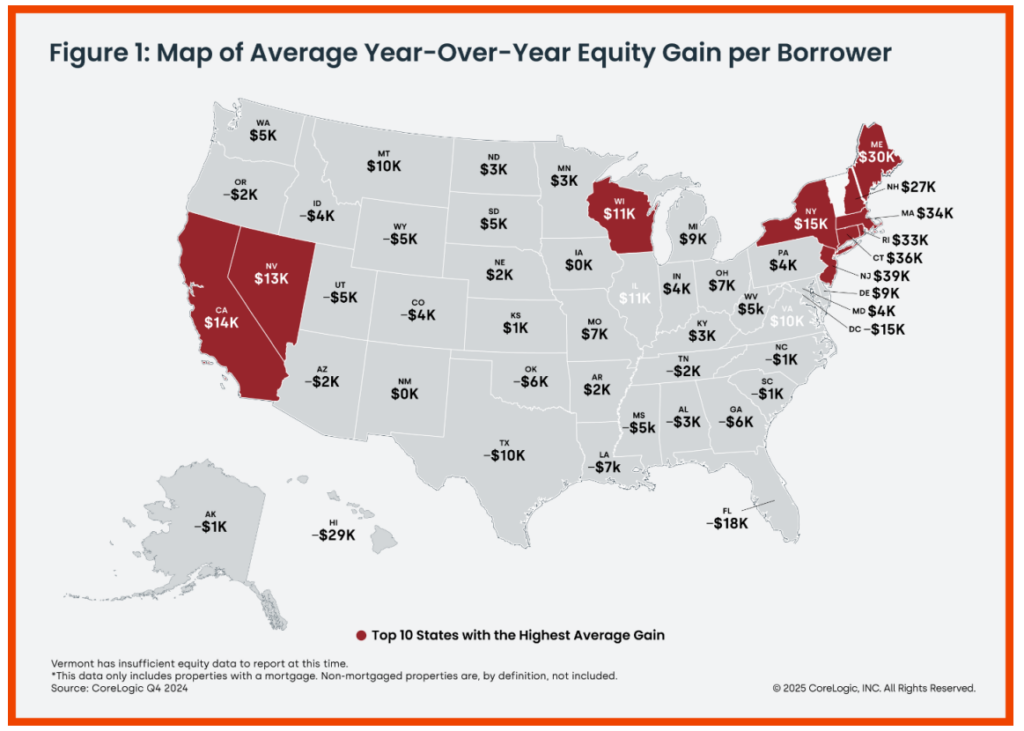

CoreLogic has issued its Homeowner Equity Report (HER) for Q4 of 2024 which found that nationwide, borrower equity increased by $281.9 billion, or 1.7% year-over-year. CoreLogic’s HER shows that U.S. homeowners with mortgages (which account for roughly 61% of all properties) saw home equity increase by about $4,100 between Q4 2023 and Q4 2024, which is less than the gain of $6,000 in Q3 2023. The states that reported the largest gains in equity included:

- New Jersey ($39,400)

- Connecticut ($36,300)

- Massachusetts ($34,400)

Conversely, CoreLogic found the states reporting the largest losses were:

- Hawaii ($-28,700)

- Florida ($-18,100)

- District of Columbia ($-14,700)

Quarter-over-quarter, the total number of residential properties with negative equity increased by 9.3% to 1.1 million homes or 2% of all mortgaged properties. While year-over-year, negative equity increased by 7% from one million homes, or 1.8% of all mortgage properties.

“Housing equity growth slowed in 2024 versus 2020-2023 due to moderating price appreciation, but homeowners maintain substantial equity gains from prior years, preserving their strong financial position,” said Dr. Selma Hepp, Chief Economist for CoreLogic.

While home equity is still boosting homeowners’ wealth, home price appreciation is leveling off and tempering equity gains for homeowners across the U.S. In fact, there are clear regional divisions for equity gains. The Northeast continues to lead the way, with other areas of expanding equity encompassing the upper Midwest as well as California and Nevada. Areas with the largest declines dotted the country, but Florida and Washington D.C. were notable areas with decreases.

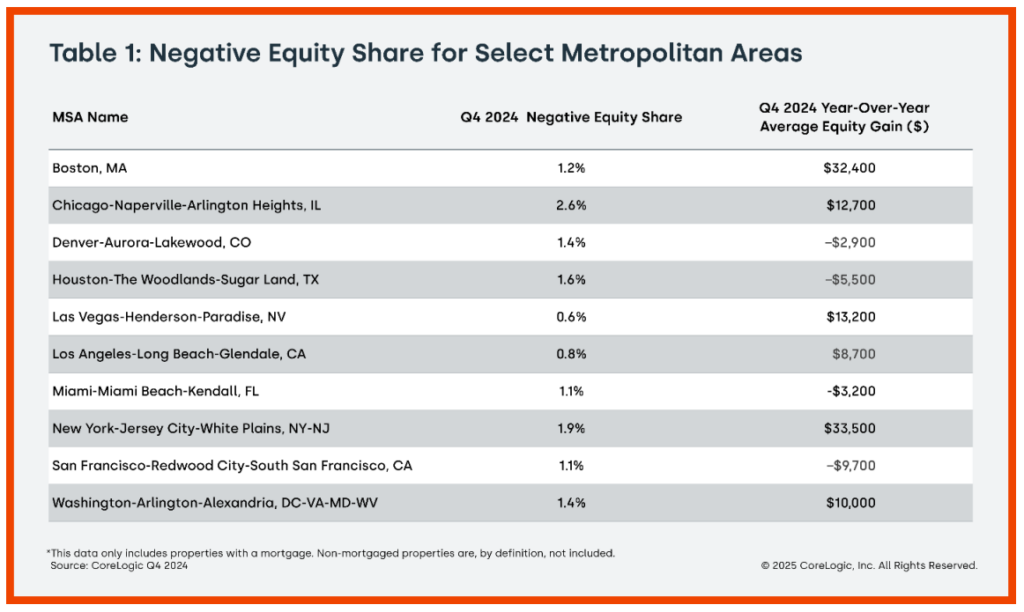

Amassing equity does not necessarily stave off the possibility of being underwater on a mortgage. In Chicago, average year-over-year equity gains were just north of $12,000, but 2.6% of properties reported negative equity. Nevertheless, past years of rapid growth have left many homeowners with a substantial accumulation of equity. This financial padding can serve as a backstop in the event of a relocation or job loss.

Housing equity growth slowed in 2024 versus 2020-2023 due to moderating price appreciation, but homeowners maintain substantial equity gains from prior years, preserving their strong financial position.

Home prices continued to be the major driver of equity shifts and markets with declining prices generally saw fallen equity in 2024. In particular, a number of Florida’s markets, including Cape Coral, Sarasota, Lakeland and Tampa have experienced weakening prices over the past year, which led to Florida’s average equity declining by about $18,000 at the end of 2024. Thinking ahead, in light of mass government layoffs in Washington metro region, it is important to note that borrowers in the tri-state area have accumulated between $261,000 (in Maryland), $287,000 (in Virginia) and $353,000 (in Washington DC), in average home equity which will help as a financial buffer but also provide a downpayment in case of a move.

Underwater mortgages apply to borrowers who owe more on their mortgages than their homes are currently worth. Negative equity peaked at 26% of mortgaged residential properties in Q4 2009 based on CoreLogic equity data analysis, which began in Q3 2009.

The national aggregate value of negative equity was approximately $338 billion at the end of Q4 2024, up quarter-over-quarter by approximately $12.8 billion or 4% from $326 billion in Q3 2023. Year-over-year, it was also up by approximately $12.8 billion or 4% from $326 billion in Q3 of 2023.

Click here for more on CoreLogic’s report on home equity trends.