In January, more home sellers emerged as fresh data suggested they are either in the process of selling or are already in the market. In comparison to the previous year, the number of homes listed for sale increased by 7.9%, according to the latest Realtor.com Housing Report.

The increase in inventory caused the median listing prices to rise 1.4% from the same period last year, while the amount of time homes were on the market decreased to more than two weeks less than before the epidemic.

“We are seeing increases in inventory and, importantly, gains in newly listed homes for sale indicating sellers are more ready to make moves. Time on market fell, signaling that buyers are ready to make offers on these new options,” said Danielle Hale, Chief Economist of Realtor.com. “While the drop in mortgage rates since last fall has helped boost buyer purchasing power, rates may not fall as quickly in the months ahead, and the anticipated improvement in affordability may be more uneven.”

New Listings Increase in January

More than half of the 50 metros included in the analysis saw new listings increase over the previous year in January, with some of the largest growth happening in Denver (+21.3%), Seattle (+20.6%), and Miami (+20.2%). On the flip side, there were places that also saw declines in new listings, including Chicago (-16.4%), New Orleans (-14.7%), and Philadelphia (-12.9%).

Homes Are Spending Less Time on the Market

Compared to January 2023, the typical home spent four fewer days on the market. In some spots, the time spent on the market decreased even more, with Las Vegas (-19 days), Phoenix (-14 days), and San Francisco (-13 days) seeing the most decline.

Other areas saw an increase in time on the market, including Indianapolis (+6 days), New Orleans (+4 days), and Birmingham, Alabama (+3 days). Only a handful of markets saw an increase over the typical 2017–2019 pre-pandemic time on the market.

These include:

- San Francisco (+9 days)

- Seattle (+9 days)

- Denver (+7 days)

- Portland, OR (+4 days)

- Austin, Texas (+3 days)

- San Antonio (+3 days)

- Los Angeles (+3 days)

- San Jose, CA(+1 day)

Listing Prices Inch Higher

Buyers are looking at slight price increases and higher mortgage rates compared to last January.

The cost of financing the typical home, assuming a 20% down payment, increased by roughly $108 (5.4%) per month compared to a year ago. With this increase, the required household income to purchase the median-priced home went up by $4,300 to $84,000 before accounting for the cost of tax and insurance.

However, as interest rates are falling and listing price growth has remained muted, the increase in the monthly cost to purchase a home has slowed, down from 6.1% year-over-year last month to January’s increase of 5.4%.

The Overall Costs to Purchase a Home Increasing, but at a Slower Pace

With a 1.4% increase over the same period last year, the national median list price increased to $409,500 in January from $410,000 in December, indicating a little seasonal dip. The low inventory gap has been supported by listing prices, and even while new home sales have been rising, construction activity hasn’t increased to the point where it can completely close the gap.

Although the median listing price hasn’t changed much from the previous year, the cost of financing 80% of a typical home has climbed by about $108 (5.4%) each month due to a combination of a little price increase and higher mortgage rates since January. This raised the needed household income to $84,000 (before taxes and insurance) from the median price of the home by $4,300.

However, the monthly cost of buying a property has increased less quickly than in January, rising 5.4% compared to 6.1% last month, as a result of declining interest rates and moderate growth in listing prices. Although the cost of buying a house is still rising, it’s at least rising at a slower rate.

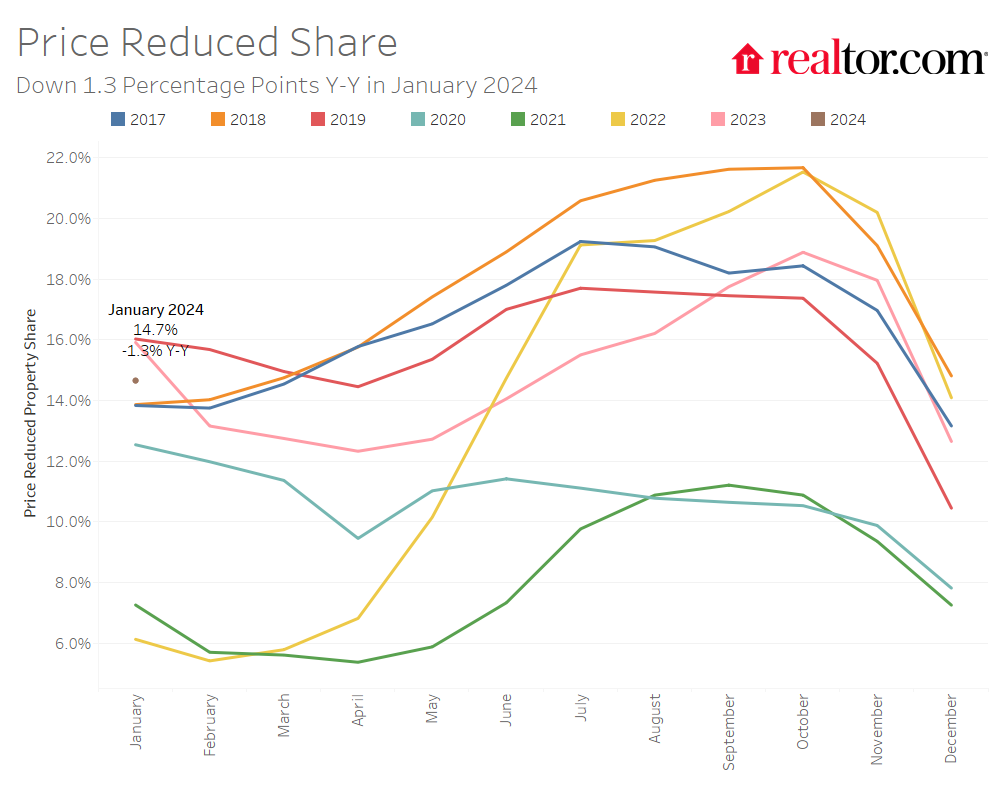

To read the full report, including more data, charts, and methodology, click here.